A mortgage loan repurchase facility (more casually referred to as a "repo") is a financing structure commonly utilized to finance mortgage loans. These facilities are utilized by both residential and commercial mortgage loan originators and aggregators to finance mortgage loans that they originate or acquire. The structure is favored by liquidity providers in the mortgage loan finance arena due to its preferential "safe harbor" treatment under the United States Bankruptcy Code (the "Bankruptcy Code"), as further described below. While exact figures are difficult to pinpoint because repurchase facilities are private transactions, based on our experience representing some of the largest players in this space, we estimate the aggregate residential and commercial mortgage loan repurchase facility capacity in the United States exceeds several hundred billion dollars.

I. Structure of Mortgage Loan Repurchase Facilities

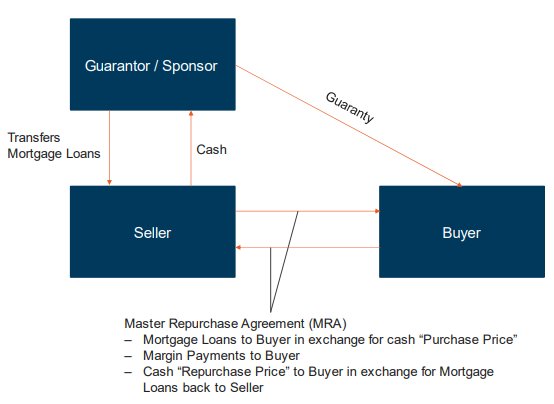

Under a mortgage loan repurchase facility, a seller (the party receiving the financing) transfers a mortgage loan or another qualifying mortgage asset (a "Purchased Asset") to a buyer (the party providing financing) against payment of the purchase price to the seller and with a simultaneous agreement by the seller to repurchase the Purchased Asset on a date certain or on demand against the payment of the repurchase price to the buyer.

Mortgage loan repurchase facilities have many of the same features as other types of secured financings. The seller (akin to a borrower) is typically required to pay monthly purchaser price differential (akin to interest). A repurchase agreement is the primary operative document evidencing this structure and contains representations and warranties, covenants and events of default that are similar to what would be found in a secured credit agreement. These facilities are further typically structured using a bankruptcy remote special purpose entity ("SPE") as the seller. A well-capitalized entity typically provides a full or partial recourse guaranty as additional credit support for the facility.

One additional, and very important, common feature of mortgage loan repurchase facilities is the ability to make margin calls. Upon the occurrence of certain trigger events (which may be credit or spread driven, depending on the terms of the specific facility), a margining provision permits the buyer to make a margin call upon the seller. The seller is then required to cure the margin call by making a cash payment to the buyer in reduction of the outstanding purchase price under the repurchase facility or, to the extent permitted by the facility documents, to transfer additional eligible assets to the buyer. The failure to timely cure a margin call would constitute an event of default under the repurchase facility.

Below is a visual representation of a typical deal structure for a mortgage loan repurchase facility.

II. Bankruptcy Code Safe Harbors

Special protections under the Bankruptcy Code make repurchase facilities particularly attractive to buyers. As a result of these protections, a buyer under a properly structured repurchase facility is not subject to "automatic stay" under the Bankruptcy Code. In practice, this means that even if a seller and/or the guarantor of a repurchase facility files for bankruptcy protection (which is typically an event of default under these facilities), the buyer can still immediately accelerate the facility, liquidate the collateral and enforce set-off rights--a clear benefit over conventional secured financings. Furthermore, unlike a normal lending relationship, payments made to the buyer under such structure are not subject to the avoidance action, except for payments made with actual fraudulent intent. A properly structured mortgage loan repurchase facility primarily relies on one of two bankruptcy safe harbor provisions--the "repurchase agreement" safe harbor or the "securities contract safe" harbor as described below.

A. "Repurchase Agreement" Safe Harbor

The "repurchase agreement" safe harbor under section 559 of the Bankruptcy Code generally requires that the repurchase transaction provide for the transfer by the transferor of eligible assets with a simultaneous agreement by the transferee to transfer eligible assets back to the transferor on at a date certain not later than 1 year after such transfer or on demand, against the transfer of funds. The safe harbor applies to a broad swath of financial assets, including in relevant part to our discussion, mortgage loans, mortgagerelated securities and interests in mortgage loans or mortgage-related securities.

B. "Securities Contract" Safe Harbor

Where the financing is intended for a period of more than one year, parties typically structure the repurchase facility to qualify for the "securities contract" safe harbor under section 741(7) of the Bankruptcy Code. A "securities contract" is broadly defined as a contract for the purchase, sale or loan of eligible assets, or any option to purchase or sell any eligible assets, including any repurchase transaction on such eligible assets. Eligible assets in this context include, in relevant part, mortgage loans, securities and interests in mortgage loans and securities.

While the safe harbor provision for "securities contract" does not have a specific time limitation, in order to benefit from this safe harbor, the buyer of the assets or its agent must qualify as a "financial institution" or a "financial participant" as such terms are defined in the Bankruptcy Code.

To qualify as a "financial institution," the buyer or its agent must generally be a qualifying banking institution, trust company or a receiver, liquidating agent, conservator of such entity, or an "investment company" registered under the United States Investment Company Act of 1940, as amended.

To qualify as a "financial participant," the buyer or its agent must either have one or more "securities contracts," repurchase agreements, or other qualified transactions with a total gross dollar value (aggregated across all counterparties) of at least $1,000,000,000 in notional or actual principal amount outstanding at the time of entering into the safe harbored transaction or when a bankruptcy petition is filed by a counterparty involved in such a transaction. Alternatively, it must have gross mark-to-market positions (again, aggregated across all counterparties) of not less than $100,000,000, in each case, at such time or on any day during the 15-month period preceding the filing date of the petition.

III. Benefits of Repurchase Facilities

The bankruptcy safe harbored nature of a properly structured repurchase facility makes this structure preferable for a provider of liquidity as compared to other financing structures. Due to the safe harbor benefits, banking institutions often also receive better regulatory capital treatment for repurchase facilities than for other types of credit facilities secured by the same types of assets. As a result, mortgage repurchase facilities are the predominantly used structures to finance mortgage loans.

Dechert LLP has one of the largest mortgage loan warehouse teams in the world, with extensive expertise in commercial and residential mortgage loan repurchase facilities. We have worked on some of the largest and most complex mortgage loan repurchase facilities, including multicurrency facilities and financings of mortgage loans in numerous foreign jurisdictions.